Three Reasons a Digital Loan Coworker Makes Sense

July 15, 2020

If you’re a lender, or in IT for a lender, you’re experiencing the changes of the “New Normal” in very specific ways. Interest rates are at historic lows – but what will that really do for mortgage demand? The Paycheck Protection Program PPP came through like a hurricane – so what’s next? My employees have been through a lot of disruption – what should I be doing for them? Well, believe it or not, a digital loan coworker may help with each of these three examples.

1) The volume example – mortages

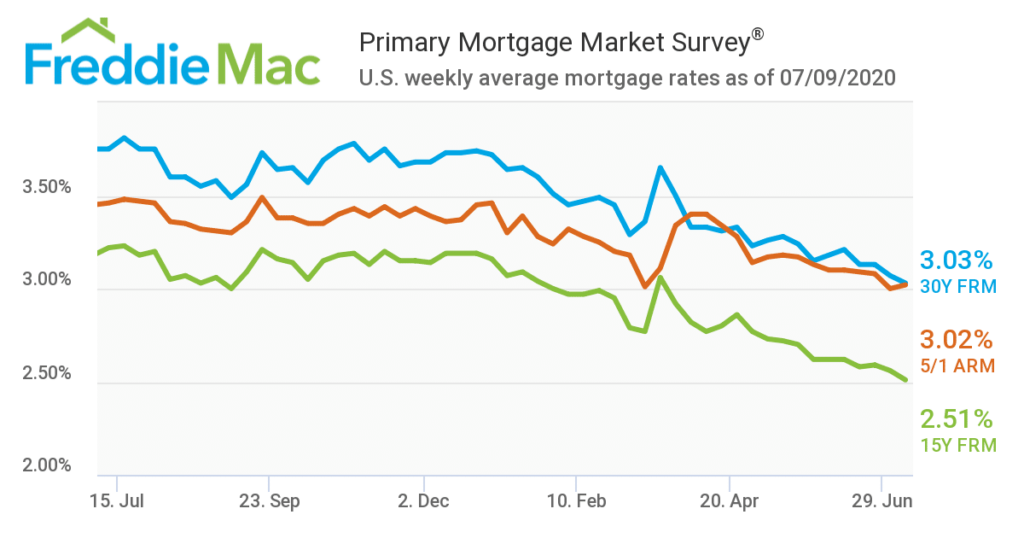

The Federal Home Loan Mortgage Corporation (Freddie Mac) reports that for the first week in July, “Mortgage Rates Hit Another All-Time Record Low – The summer is heating up as record low mortgage rates continue to spur homebuyer demand. However, it remains to be seen whether the demand will continue if COVID cases rise to the point that it hinders economic growth.” The most popular option is the fully pre-payable 30-year fixed rate mortgage (FRM), which has dropped 72 basis points in the last year to 3.03 percent.

Regardless of actual housing sales, these record-low rates are generating refinances. In its Research Note dated July 6, Freddie Mac states: “With mortgage rates reaching a then-historical low in March of 2020, mortgage refinancing activity surged at the end of the first quarter of 2020. There were nearly $400 billion in single-family first lien refinances in inflation-adjusted 2019 dollars. This is about double the volume of a year earlier…”

Matching volume / demand to your workforce size is difficult – even in the best of times. As the quote above said, there could be lots of demand – “However, it remains to be seen whether the demand will continue if COVID cases rise to the point that it hinders economic growth.” So, what should you do? There is a lot of time and cost involved in hiring and training people to assist with mortgages. Hire too many, you have layoffs; hire too few and you’re swamped. Employees working remotely adds another layer of uncertainty about productivity. A digital loan coworker can be easily added or removed to scale up or down based on volume, stabilizing your workforce needs. You can pivot quickly and efficiently – in either direction.

2) The customer service example – Paycheck Protection Program (PPP) forgiveness

Remember all those customers trying to file their PPP applications with you? The full lobby; the phone calls and emails; the nastier phone calls and emails? The long hours…the paperwork…and more paperwork. Hopefully, you survived it all and really helped your customers get the funding they needed.

But now the same glut that happened during the PPP application process may happen again as those borrows return to you – as their PPP originator – to file for PPP forgiveness.

Wanting to make it easier for businesses to realize the full forgiveness of their PPP loans, in June the SBA issued a “borrower-friendly” PPP loan forgiveness application (find it here), as well as a three-page “EZ” application that certain borrowers under specific circumstances can use (find it here). To have the whole loan forgiven, the PPP borrower must spend at least 60 percent of the loan on payroll costs within 24 weeks of receiving the loan to have the whole loan forgiven. (The remainder should be spent on mortgage, rent and/or utilities.) The 24-week period can’t extend beyond December 31, 2020. The borrower has 10 months to apply for forgiveness from the end of your 24 weeks or December 31, 2020, whichever comes first.

So, unlike the original PPP application rush, the forgiveness rush may be spread over a longer time, although most businesses would want the debt forgiven as soon as possible. Even with borrower-friendly and EZ forms, what type of service should your customers expect from you this time around? A digital loan coworker can handle a lot of things, like read emails, recognize and collect applications, forms and supporting documents; match data and perform consistency checks; and generate documents or integrate into the next process step. You’ll be able to handle the forgiveness much better than the original loan – and your customers will appreciate it.

3) The free up your employees example – every loan type, probably

Somewhere in your loan processing you’ll find some type of tedious work, like matching data between forms; or necessary, but mundane, manual work, like re-keying information between systems. This type of work can be boring, tiring, and frustrating for any level of employee. Add to this the distractions and disruptions of working remotely and other related current events, and it will be no surprise that productivity is down, and errors are up. Unfortunately, this is usually more than one person or an isolated event, and the ripples can affect your whole operation.

The digital loan coworker doesn’t find anything repetitive, mundane or tedious – it will do the same tasks 24 hours a day, quickly, with an extremely low error rate, and without complaining. Once programmed, it never needs a refresher course, no additional training is needed for updates or changes. A digital loan coworker easily bridges non-integrated systems or information “silos,” and the mundane rekeying is gone. The digital loan coworker is not intended to replace employees – even lower level or entry workers. It’s meant to free up those employees for more important work and projects – to the benefit of all of you.

Prolifics can help

The “New Normal” is here. You have a vision – don’t let your technology slow you down. You must be relentlessly efficient, scale to volume in a heartbeat, and squeeze out costs wherever you can. This is where digital loan coworkers can make an immediate, positive impact with minimal implementation and little, if no, disruption. Prolifics’ digital workers, like Archie, your digital loan coworker, will get tasks done quickly, accurately and completely, freeing up your employees for more important work. Visit www.prolifics.com or email solutions@prolifics.com.